Focused Investing Perspectives #55: TIPS!

At the moment it is worth being aware of Treasury Inflation-Protected Securities.

I wrote the following for my kids this morning, then decided to share a lightly edited version here.

I have been averse to bond investments for much of the past decade. Since bond prices fall a lot when interest rates rise, this was particularly significant when rates were low. And indeed bonds lost a lot of value in 2022 as rates rose.

Today I still oppose target date retirement funds because their "bond" investments are in bond funds. Those funds churn their investments and so lock in losses when their holdings drop. If you want to hold bonds, the only sensible way to do it is to own individual bonds and hold them to maturity.

Of particular interest at the moment is TIPs. These pay a regular coupon and in addition their principal increases with inflation. Because of how that is taxed, you only would want to hold them in tax-deferred accounts.

So long as you held the TIPS to maturity, you would get that yield and that real return and get paid out the inflated principal at the end. But if TIPS yields were to rise, then you would have to take a significant loss to sell. At the moment, 30-year TIPS issued in 2021 at very low rates have lost a third of their value even after inflation.

TIPs that mature in 20 years or longer pay 2.5% today, a high. So if inflation averages 3% over that period, the annual return is 5.5%. This does not sound like a lot, but there is a good chance that stocks on average will not do even that well over the coming 20 years.

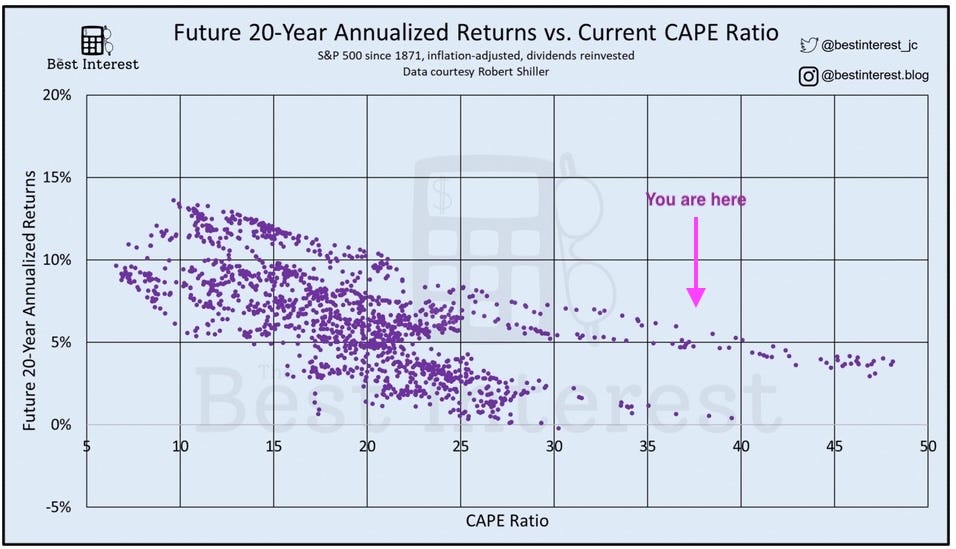

You can see the historical outcomes in this plot from the blog Best Interest:

In two of the three historical cases (in more than 150 years) where the CAPE ratio has gotten this high, the forward return was 5%. But most historical peaks only go to 27 or so, and they ended up with much lower forward returns. Having money today in an S&P 500 index fund represents a guess, deliberate or not, that “this time is different.”

So if you have money you are ready to lock up for 20 years or more, and you are not a stock picker, TIPS are the more-secure alternative to stocks.

In my opinion, right now TIPs are a more certain way to store and increase long-term value than gold or bitcoin. So if you want, as part of your overall planning, to set aside some value to get a guaranteed 20-year return, this is a good time for them.

My personal timescale is too short for me to take this path now. The 5-year TIPs only pay 1.5% and the 10-year pay 1.9%. That said, if I wanted to (or had to) stop actively investing I would likely put some money into them.

Member News

Looking Ahead

I’m nearly done with my workup on Equity Lifestyle (ELS) and should have it out in a few days. Paid members will also see a monthly update.

After that, as usual for major holidays, I will be absent from the chat and not publishing (unless I can’t help myself) for a week. The next Perspectives will be in mid-July.

If you are in the US, enjoy the holiday.

Recently published material

Material in the past month has included the following 13 items. You can see it all, and search it, at https://focusedinvesting.substack.com/

Recently:

Deep dives with no paywall on Tourmaline Oil, Front View REIT, and Kite Realty Group

Deep dives with a preview on VICI

Six Brief Notes

On EOG resources, on macroeconomics, and on Canadian REITs, and on a dissonant aspect of coverage of CRE, to all subscribers.

On some price action and on Orion Properties, to paid subscribers

One Trade Alert, exclusive to paid members.

A monthly update, with a preview

Paid members also have access to the Focused Investing Chat.

Other Resources

To find my past articles covering a given company, go to the Focused Investing home page. There is a search function to help look for past articles. Search by name or ticker.

A note on my approach to restricting access: Anything providing details of my trades and portfolio is restricted to paid subscribers, as is anything I consider to be immediately actionable. Most articles with information it seems members may act on have a preview section followed by a paid section where the real meat is.

The Google Sheets (for annual members):

The main attraction on the Google sheet is full disclosure of my live, real-time portfolio. If you are an annual paid member and do not have access, please contact me.

There are in addition a REIT assessment sheet, some data from NAREIT’s REITWatch, and a Midstreams assessment sheet, each a tab. And if you scroll down on the Current Portfolio tab, you can see limit orders, some tickers I track, and some playing with possible portfolios.

Also:

Paid members can also post items of interest on the Focused Investing Chat, which I do often. Check it out and post your own items, please. Comments and questions are always welcome.

It can be challenging to search the chat (for paid members only) or to find past articles on mobile devices. To do so, you have to get into the chat so my picture is on the top left, and then punch my nose with your finger (ouch?). You will see a display with a search emoji and a link to the home page where you can search.

Please click that ♡ button. And please subscribe and share. Thanks!