Scenarios for TIPS

Details about TIPS and how they can be useful, or not.

In considering whether to use Treasury Inflation-Protected Securities (TIPS), and communicating a bit with subscribers, it became clear that some general information and discussion would best precede my personal story. So this is something of a tutorial.

We can begin with context from my experience. Harry Brown was a famous and successful investor in the 1970s and only later turned to politics. I subscribed to his newsletter, which came with a big three-ring binder and was printed on three-hole-punched paper.

Looking backward from 1980, economic and financial possibilities seemed quite fraught with risk. Having studied developments in the 20th century, Harry’s view was that a real (i.e., inflation-adjusted) return of 3% was excellent and was what one can sensibly seek. He also was big on preparing for various worse cases.

Then, thanks to the actions of the Fed, led by Paul Volcker, inflation was vanquished. Bonds began a 40-year bull market. During all that time it was feasible to seek real returns far above 3%.

Today we have again entered tougher times, but almost nobody remembers what they were like. It is worth recalling that inflation in the US was more like 2% than 0, even in the good times. So an earnings growth rate of 5% was actually a real growth rate of 3%.

This all sets the context within which we should view the story of TIPS.

A Significant Development

Today long-dated bond yields are near 5% for Treasuries and are 5.5% plus for A-rated corporate bonds. This is not bad and a retiree could sensibly set up a bond ladder for income.

But what seems really significant to me is that yields on Treasury Inflation-Protected Securities (TIPS) are above 2.5%. This gets you total returns of 4.5% for inflation at 2% and steady TIPS yields. I will explain how this works below.

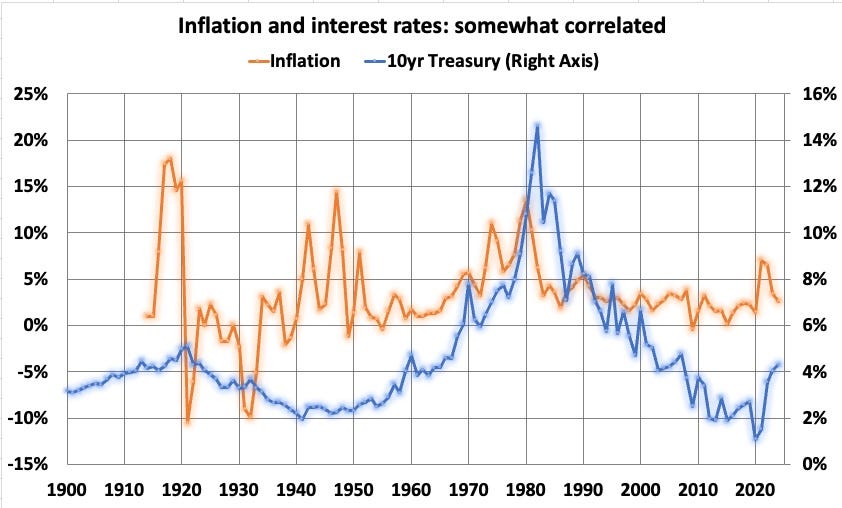

Those standard bonds will not see their interest payments change if inflation goes to 4%, while the TIPS will then return 6.5%. TIPS provide some protection against a period of extreme inflation (by US standards). And one of the really big worries for retirees is a burst of inflation that rhymes with the 1970s, which you can see here:

There are reasons to think the Great Inflation was a one-time event, but you never know. During the Great Inflation, inflation was above 5% and (a bit lagged) treasury rates were above 8% for more than a decade each. I had relatives who saw the value of their fixed, pension income drop by half from retirement to 1982.

Details on TIPS

TIPS are unique securities. It is easy to get confused about how they work. Here is the summary from Treasury Direct:

We sell TIPS for a term of 5, 10, or 30 years.

Unlike other Treasury securities, where the principal is fixed, the principal of a TIPS can go up or down over its term. [Pursuing the examples shows that the change in principal from the issued value is the ratio of current CPI to CPI on issuance.]

When the TIPS matures, if the principal is higher than the original amount, you get the increased amount. If the principal is equal to or lower than the original amount, you get the original amount.

TIPS pay a fixed rate of interest every six months until they mature. Because we pay interest on the adjusted principal, the amount of interest payment also varies.

You can hold a TIPS until it matures or sell it before it matures.

There is also an important hitch. The IRS treats any increase in principal as current, taxable income. If that income is taxed, the taxes can reduce the total returns below the rate of inflation. So unless you have very low taxable income, TIPS should be bought from tax-protected accounts.

You can purchase TIPS directly at auction but it is likely more convenient to buy them in the secondary market. TIPS have some unique jargon that can be confusing. Let’s look at a screen from Fidelity, showing two securities:

The key numbers in the description are the coupon yield and the maturity date. These are repeated in the third and fourth column, with the coupon shown as a percentage. There are no call dates and the ratings don’t matter.

Focus next on the unshaded column entitled “Inflation Factor” between the two regions shaded gray. This shows the ratio of the current CPI to the CPI on issuance. More below on this.

Now consider the columns shaded gray. The “Price” is the percentage of the face value bid or asked. But because the principal has been adjusted for inflation, what you actually pay, as a percentage of face value, is the “Price” times times the inflation factor. That is shown as the “Adjusted Price.” [So complicated! I swear, only a bond guy could love this.]

The line shown below the price is the top of the “book” of offerings. It shows shares available at that price and the minimum lot required to get that price. Your broker will have a way to see the “Depth of Book” which will include a range of minimum shares and ask prices.

Finally, the Yield to Maturity (YTM) is just what it sounds like. The Adjusted Price is the Net Present Value (NPV) of all future payments, including the final payment of principal, discounted at the Yield to Maturity.

Components of Returns

In contrast to common stocks, that Yield does not all come to you as a coupon payment. Using the bond in the top row above as a reference, the coupon yield right now is the ratio of the coupon to the nominal Price (and also equals the ratio of the full interest payment to the Adjusted Price). For this example, it is 1.93%.

So what gives? The YTM is 2.6% yet you only get 1.9% in the coupon? Yep.

If you are using the TIPS for income, this is really important. Your assured cash return is just the coupon and is smaller than the return implied by the Yield to Maturity.

I have to confess that, not having previously focused on TIPS in any detail, this is a disappointment. But remember that the coupon is the coupon yield times the inflation-adjusted face value. This helps a bit.

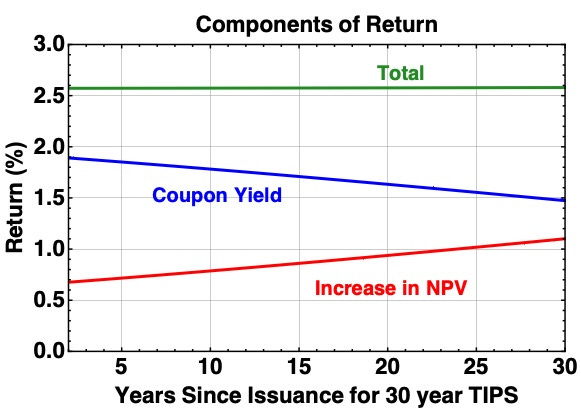

Overall, there are three components to your return. These are the coupon, the increase in Net Present Value (NPV) of the future payments, and inflationary increases in principal. The second and third of these can only be realized by selling part of your position. Let’s look.

The first two of these turn out to add up, at least very closely, to the Yield to Maturity. Here, for our reference bond, is how that works:

The NPV increases as the year gets closer to maturity, because the final principal payment is closer. The Coupon Yield drops in response to the NPV increase.

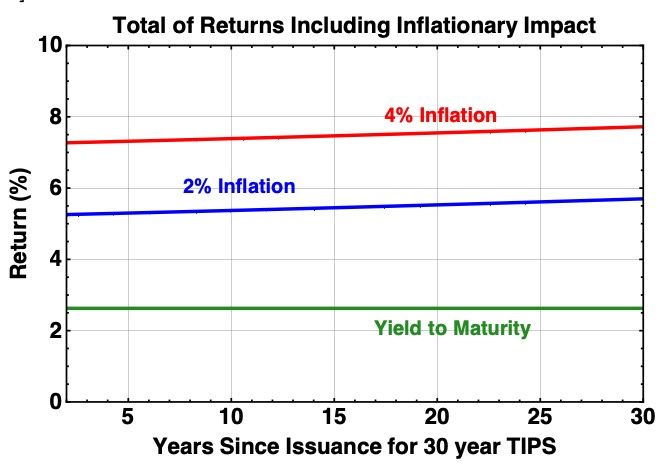

The inflationary increase of principal increases also increases the interest payments. In combination, these boost the returns, mostly by increasing the principal value. The total of all returns is roughly the Yield to Maturity plus the inflation rate. Doing the actual calculation, I find something a bit larger, with results shown here:

One can overdo the details, since neither the actual rate of inflation nor the Yield to Maturity that the markets will set is predictable or fixed.

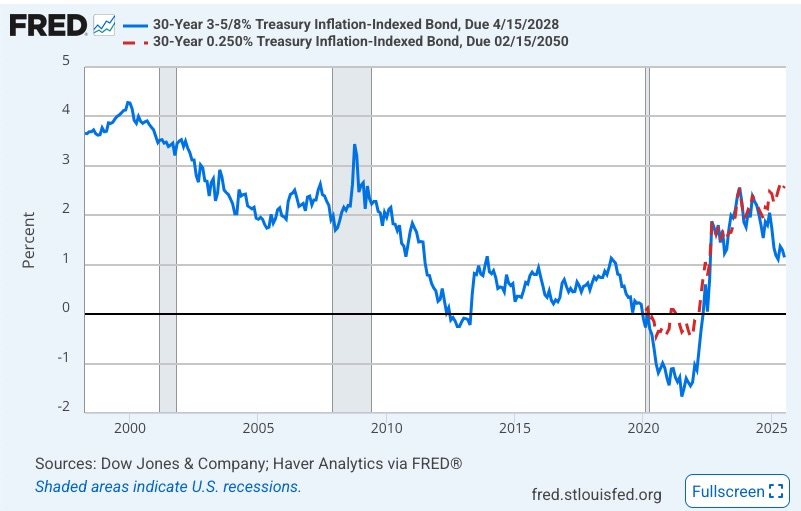

Those market yields have varied markedly, as you can see here:

An investor who bought the TIPS issued in 1998 soon thereafter got an initial total return near 6%, and gained much more income via inflation, with a bump as inflation surged in the early 2020s. The inflation factor today is about 2x for that security. But if that investor needed to sell in 2021, he lost his shirt. An investor today might potentially make a real killing if there is a return to low interest rates.

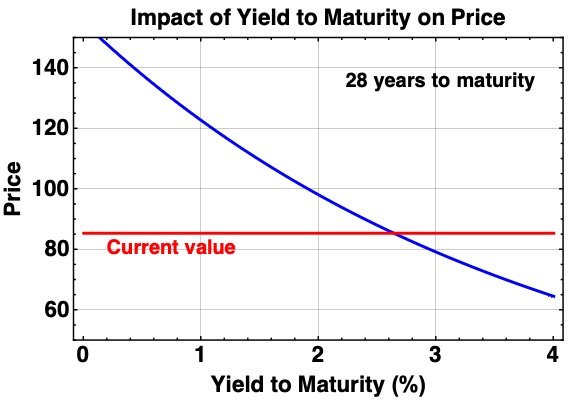

Here is how the NPV of our reference bond would change as the market changed the Yield to Maturity:

We see that if the YTM goes up by a third, the price would drop by something like 15%. But if the YTM drops to a bit below 1%, as was true throughout the 2010s, the price will go up 50%.

In summary, there are three key points about long-dated TIPS:

No matter what interest rates do, they will keep paying.

What’s more, those payments will increase by the amount of the inflation rate.

And if interest rates drop markedly, then the price of long-dated TIPS will go up a lot. This may happen in a recession when the stock market is also likely to be depressed, providing great opportunities.

This combination of inflation-adjusted returns and potential anticorrelation with stock prices is a unique selling point.

Scenarios

It seems to me that current circumstances are a good setup for those who buy these TIPS. Let’s consider some scenarios.

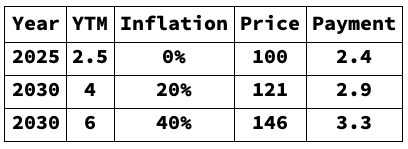

Inflation and interest rate increase

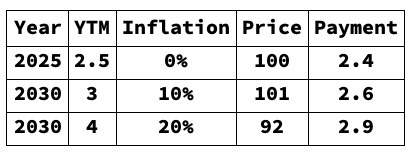

Suppose the next 5 years see some amount of inflation and also an increase in YTM. Here is a comparison of a couple possibilities with initial TIPS bought this year. Price is shown as a percentage of your purchase price.

If inflation over the next 5 years totals 10% (roughly 2% per year), and the YTM increases modestly to 3%, then the TIPS will have a 10% increase in payment and a 1% higher value. (Remember, part of the return is the increasing NPV, for flat YTM.)

If inflation over the next 5 years totals 20% (roughly 4% per year), along with an increase of YTM to 4%, then the TIPS will have a 20% increase in payment and an 8% lower value. You still might choose to sell that TIPS to buy something down, say, 30%, if there is a bear market.

Sterotypical recession

Here economic activity contracts and the Fed pulls interest rates down in response. TIPS YTMs and stock prices likely drop. Dividend growth slows overall, with exceptions — some are cut and others still grow strongly. Inflation is not certain, but might stay low, especially at first.

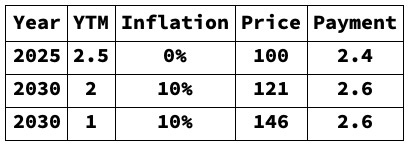

Consider the same 2025 TIPS but now suppose YTM drops to 2% or to 1%. Here is what happens:

The sensible move here would be to sell some TIPS and invest in solid companies whose yield has been driven up. The TIPS represent a way to gain from the same circumstances that produce the high yields.

Stagflation

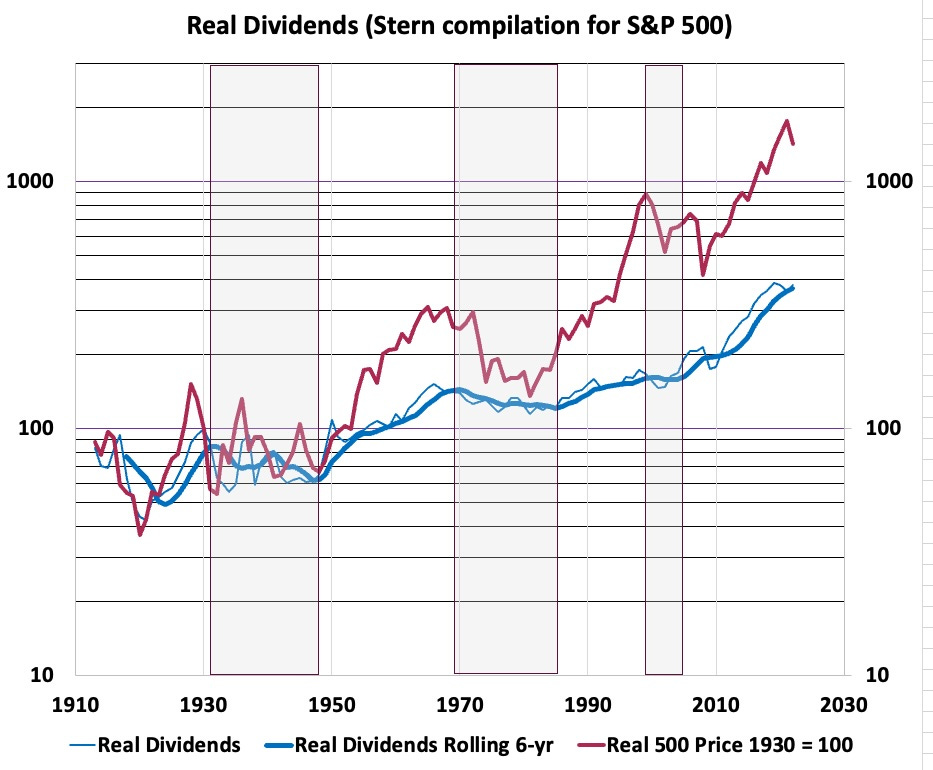

This word is overused today, but has meant the combination of a stagnant economy with significant inflation. Real (i.e., inflation adjusted) dividends may stagnate or drop; they dropped a bit overall across the 1970s:

For the TIPS, the inflation increases the nominal yield and in such a scenario this might matter. Here are cases where the YTM increases to 4% or 6%, in response to inflation of 20% or 40% over the next 5 years:

Here you get the increase in interest payments and you may need it. You might still get compelling opportunities to take a loss on some TIPS and buy equity income on the cheap. That, however, is hard to predict.

Takeaways

TIPS are a different way to invest, with some advantages. They do represent a good option if you want to see gains from falling interest rates so you can use them to buy stocks that are down.

However, today the coupon yields remain depressingly small. Owning a TIPS today with a Yield to Maturity of 2.6% but only a 1.9% coupon yield is in some way like owning a company paying a 1.9% dividend and buying back 0.7% of the float per year. The main problem is the same: the markets may or may not give you that 0.7% any time soon.

One can take advantage of the return of inflation-adjusted principal at maturity by buying TIPS with shorter maturities, perhaps in a ladder. But you get a smaller YTM doing that. At the moment the highest YTMs for 2030 TIPS are near 1.5% while those for 2035 TIPS are near 2%.

My next project is modeling how holding a high fraction of TIPS would change my projected portfolio performance going forward.

Please click that ♡ button. This helps push Focused Investing up on the Substack feed. Also please restack, and share. Thanks!

I will be saving my Sunday morning coffee time to review your analysis on TIPS! It's not an investment I have spent much time on but now seems like a good time to learn a bit on the subject. Thanks!

Thank you Paul.. I'm still a little confused. Need to read it again. I want to better understand how the return (market price) (positive or negative) on the TIPS compares to buying a zero or 30 yr treasury at the same time under the same scenario. Can you please do a direct comparison. If you buy a 30yr bond today at par with a 4.75% coupon and in 5 years long term rates go down to 3% your 30 yr bond with a 25 yr remaining term will go to about 130% of par..If rates trend the other way to 6.5% then your bond will be worth about 78% of par. I understand there are other differences between the types of investments but I want to understand this comparison first. Given the disparity in"coupon rate" at the beginning I'm not sure what type of change in rate would be fair comparison for the TIPS given the other variable but I'm guessing you would.