Devon Energy

There is a lot of opportunity today in upstream oil producers. Mr. Market has left the building. Is this one — Devon Energy — worth buying?

The Company

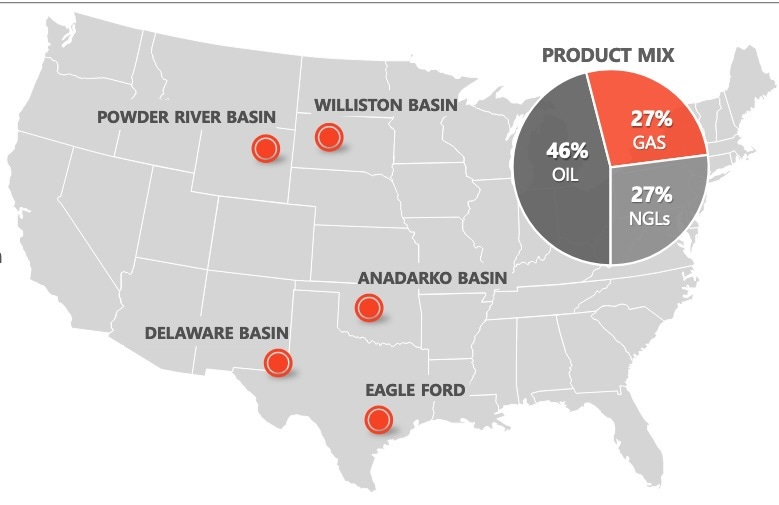

Devon is a moderately sized, multi-basin producer of oil and other hydrocarbons. Here is their portfolio map:

Note that the product mix shown is on a BOE basis, which is standard in the industry but also misleading. For Q3 2024, on a realized price basis, the fraction of revenue contributed by natural gas is 4% and that by NGLs is 12%.

They claim more than 10 years of development inventory and multi-decade total resources. This is the usual confusion where there are different flavors of “inventory” or “resources” that reflect different levels of research on what can be produced.

These days oil producers are increasing inventory mainly through acquisitions. We will see below how Devon just did that.

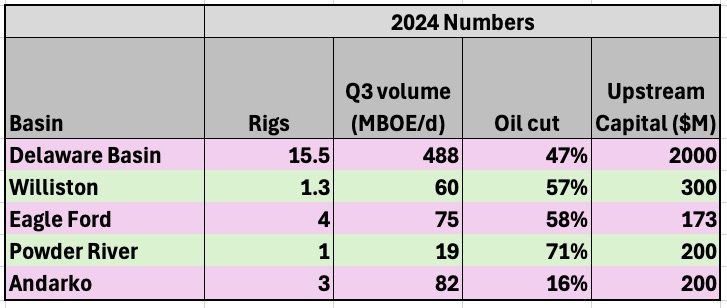

Devon provides nice detail on each basin where they work in their November presentation. Here are some relevant numbers for Q3, 2024 (MBOE/d is thousands of barrels of energy per day):

This translates to oil production of about 380 MBO/d, which is also their preliminary projection for 2025. This is 19% larger than the 320 MBO/d they reported in Q1 and for 2023.

So oil production will have been about 10% larger for 2024 than 2023 and will be another 10% larger in 2025. As is detailed below, the associated dilution is 8% so the value/share increase (at constant oil price) is about 12% even as the share price has dropped by about a quarter. Since the dilution was this year the value increase nearly all comes next year.

You can see here in the table it is the Delaware Basin (within the Permian) that dominates their production volume. Elsewhere, the recent acquisition of Grayson Mill (discussed below) is increasing their Williston basin production to 150 MBOE/d and sustains their overall 10 years of inventory in that basis.

Like most producers, Devon is steadily increasing their efficiency. In response, the number of rigs they are running is coming down. They are more oriented toward sustainable production than production growth.

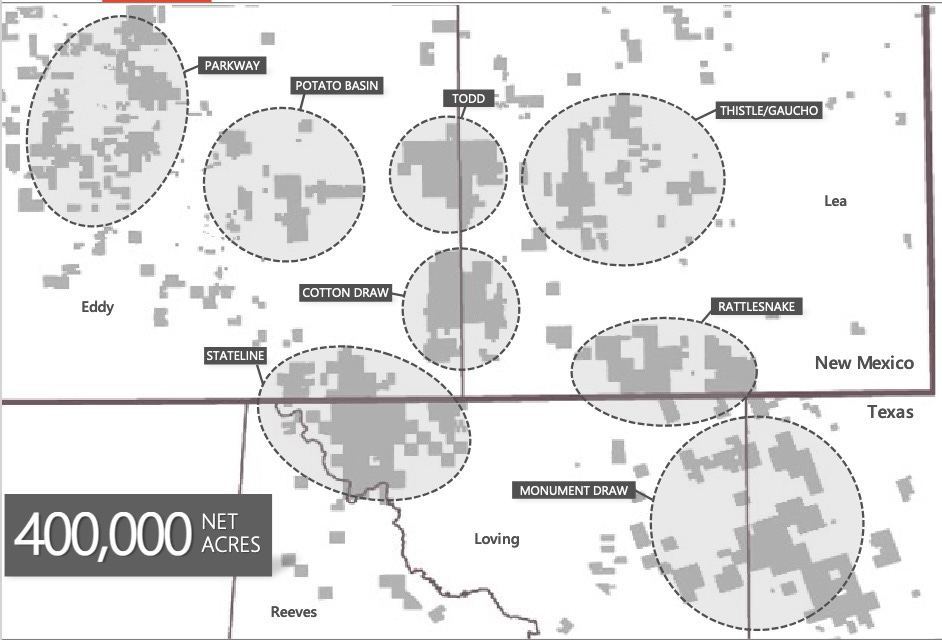

Beyond the numbers, their Delaware acreage lies near the intersection of Eddy and Lea Counties in New Mexico with Loving County in Texas. This is high-quality rock in a stacked play.

For the economically proven locations they will drill over the next 10 years, the breakeven oil price is $40/bbl. They also highlight their multi-decade inventory in the Delaware.

Details vary across their other basins (see the presentations and other filings), but mostly are not worth our time here. Andarko, an older play, has a smaller oil cut. Eagle Ford, another older play, has a lot of “refrac” opportunities.

The big change in the past year was the purchase of producer Grayson Mill in the Willison Basin. This tripled their production there with no loss of resource depth.

To make that purchase they issued $3.3B of new debt and issued $1.8B of new stock, a dilution of about 8%. With an oil production increase above 14% that was a good deal.

As to their long-term plans, Devon addressed these in an interview with Seeking Alpha service High Yield Investor:

“Our goal is to maintain flat production levels while improving efficiency. Last year, we had a 12% improvement in completion efficiencies and a 14% improvement in drilling efficiencies.”

In the world of oil today, this approach makes enormous sense to me. Next let’s see what the finances have to tell us.