Brief Note: Essential Properties

If you read one investor presentation this year from a listed REIT, particularly in net lease, read one from Essential Properties Realty Trust (EPRT).

I got curious about the material released yesterday. This is such a thoughtfully constructed and well-run REIT, so no wonder they are so highly valued.

But they are still young and have a couple questions to answer going forward.

Who is Essential Properties?

Essential is still a young REIT, and growing rapidly. Some highlights:

Entirely triple-net leases; nearly all sale leasebacks

About 2,000 properties, 99.7% leased

An emphasis on service and experience based tenants for e-commerce resistance

Financial reporting at the asset level throughout.

Same store rent growth of 1.4%, typical for this class of property

Average asset is small, at $2.9M, enhancing fungibility.

Closing about $300M of investments per quarter

Dispositions at about $30M per quarter, nearly all occupied when sold.

Here are what they see as highlights:

These are good numbers. There is not really a mystery here.

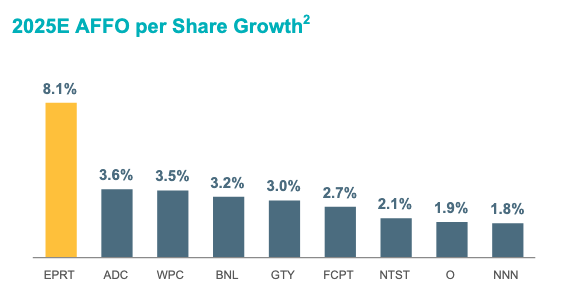

Essential is growing earnings far faster than their peers. For most net-lease REITs including this one, AFFO is a reasonable approximation to cash earnings.

This high growth comes in part from having a sector-low payout ratio on AFFO of 66%. They can lever the retained cash up to 50% of AFFO and invest that at say 8% to get 4% growth of AFFO on top of that 100 bps from rent escalators.

In addition, the high stock price awarded them by the market lets them generate more growth by issuing stock (across 2024 they increased the share coung by 15%). On top of that, they do not (yet) have the headwinds that are reducing the rate of growth of most REITs today.

[This is the ballpark growth story; I did not dig for the precise numbers.]

Uncertainties

But there are uncertainties.

Diversification.

Essential chose to invest in only 16 industries, to be able to maximize their experties and reap the benefits. So on average that would be 8% of Annual Base Rent (ABR) per industry but of course this is distributed:

What gets all the attention here is car washes, which are a popular industry to hate at the moment. Essential adeptly shed nearly all of their Zips Car Wash properties well before the recent bankruptcy, and the three they still own are current in rent. But that 20 bps of ABR remains at risk.

The critics claim that an implosion of that industry is coming. If so, we will see how well Essential weathers it.

Debt Ladder

Essential carries a Debt Ratio, at 35%, which is outstanding for this type of REIT. But their average debt maturity is short, at 4.2 years. Plus it is in term loans through 2030 before their first public unsecured bonds mature in 2031:

There is nothing wrong here; they are just young. And they, so far, have the advantage of not seeing interest costs increase from having to roll debt in addition to adding new debt.

Here is more on that: They have been adding about $400M of debt per year as they grow the portfolio at $1200M per year. But they need to replace that first $400M tranche, ideally later this year but for sure next year, to keep their protective period without refinancing.

[The leaders of Essential have a lot of connections with Chris Volk and so with STORE Capital and its predecessors. So I will draw some contrasts with his business model, which included such protection.]

Starting soon, Essential has three choices:

They can go rapidly out further with their debt ladder, pushing it out two years per year. NNN REIT (NNN) is out well beyond 10 years, but NNN has a higher credit rating and more credibility generally.

They can start doubling their maturities per year, by placing new debt at twice the previous rate. But that would push up their Debt Ratio add a lot of balance sheet risk over time.

They can pay off the maturing debt. This was the approach Chris Volk favored: dispose of enough property in any year to pay off the maturing debt.

It will be fun to see how they handle this.

Takeaways

Essential Properties does seem like a nice variation on the model of STORE Capital. But their deliberately narrow subsector focus adds concentration risk to reduce e-commerce risk. They are large enough now to add a couple new subsectors, which would be good.

The big question is what their long-term approach to debt will be. The growth rate they can sustain is likely to drop some as they implement a path.

So far they have been doubling Gross Assets every three to four years. They have 3 or 4 more doublings before they reach the diminishing returns that Realty Income (O) is seeing. That should take one to two decades.

Looking at discounted cash flows, I don’t see EPRT as undervalued. But I do think they are likely to sustain their dividend and grow it rapidly.

Please click that ♡ button. And please subscribe, restack, and share. Thanks!

Thank you for sharing your take on EPRT. Sorry, English is not my native language, I did not quite get what you meant to say in the first option: "They can go rapidly out further with their debt ladder, pushing it out two years per year". Can you please clarify?

Thanks for this write up. You have peaked my interest as a potential "growth" REIT. I am going to put it on my radar for any significant weakness.