Brief Note: Crown Castle

Thoughts on Crown Castle REIT.

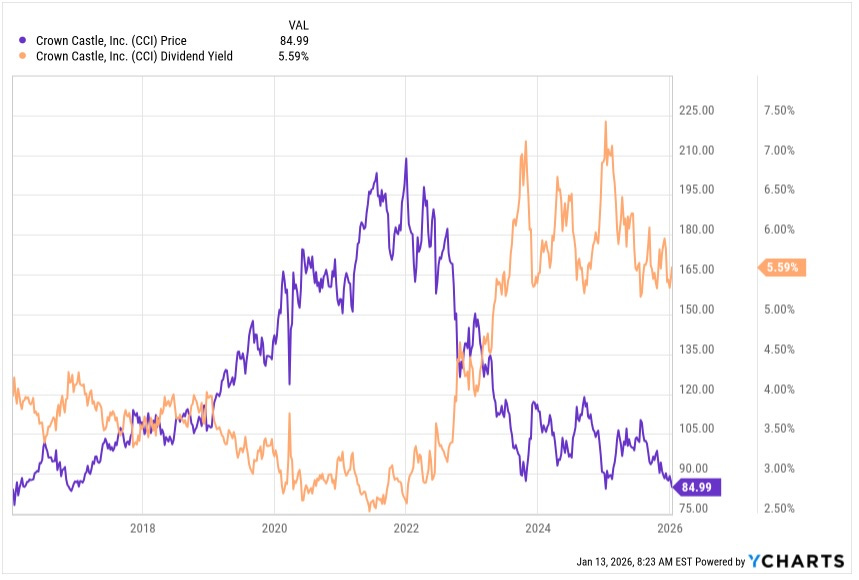

Some of my subscribers have wanted my thoughts on Crown Castle (CCI) for awhile. No wonder, with their dividend yield having climbed above 5% as the stock price dropped nearly 3x:

My thoughts may not be worth much, but here they are.

Crown Castle has a pending sale on their fiber assets and is transforming to a pureplay US cell-tower REIT.

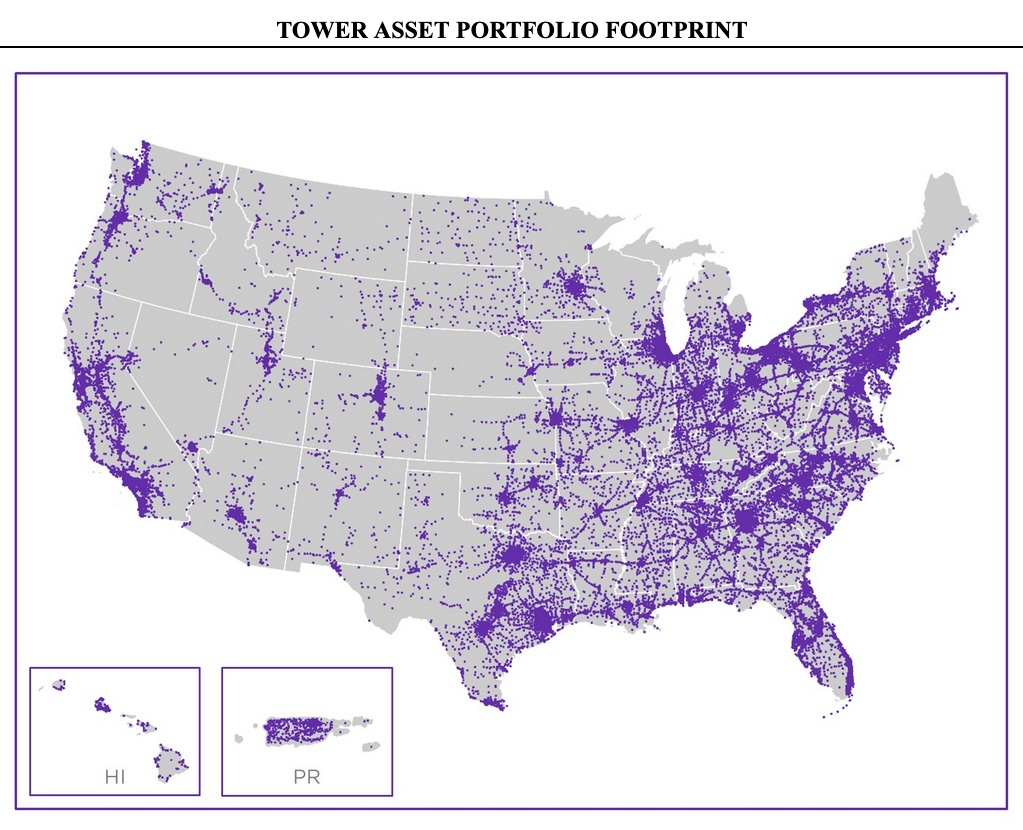

Tower REITs are atypical REITs. Their towers span the US, as you can see here:

Tower REITs are an unusual type of REIT. They are less involved with the real estate itself.

Some REITs own and operate properties, leasing their use to tenants. Examples include shopping center REITs and apartment REITs.

Some REITs own properties and lease all aspects of their use to tenants, usually with triple net leases. Such REITs are at root financing operations, which enable their tenants to run capital-light business models.

Tower REITs provide services to other businesses, in this case towers and power. They may or may not own the properties that provide those services. Billboard REITs are similar. Their earnings come from payment for the use of those services by other businesses.

Notably, in contrast to retail stores leased from a REIT, tower locations are not profit centers for the telecoms. Leasing space there is like paying for parking. The rent is just a cost.

Tower REITs have long leases, which provides some stability to revenues. There is less stability in billboard REITs, where leases are short.

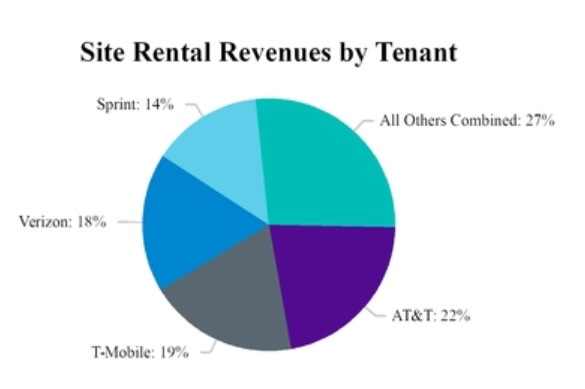

Tenant Concentration

Their most dangerous challenges arise from tenant concentration. This is severe; here was Crown Castle in 2018:

Having nearly all your revenues with four tenants carries high risk. We saw this play out with the merger of T-Mobile and Sprint, which led to large numbers of lease cancellations.

The loss of revenues from expiring Sprint leases produced roughly a 10% hit to CfO in 2025. This drops to being roughly a 1% headwind from 2026 through 2034.

It is no surprise that they exclude this from their reporting to shareholders. On an ongoing basis, they expect another headwind of roughly 1% from terminations by other tenants.

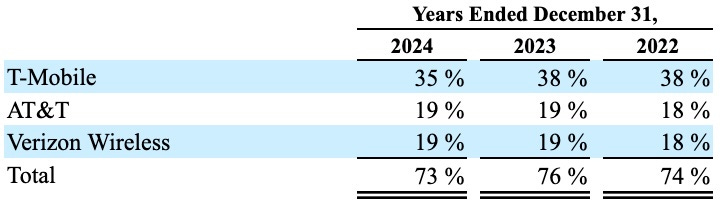

Plus, their tenant concentration got worse:

On top of the sheer numbers, the telecom industry has not been tremendously stable. They keep having to negotiate major changes and seem prone to doing mergers that don’t work out.

The latest telecom drama has been brought to us by DISH. Here is what the CEO, Christian Hillabrant, said about their tenant DISH on the earnings call December 9.

DISH representative of approximately 5% of our overall revenues, continues to pay their bills on time, of which we’re thankful, has elected to go down a route whereby they’re selling their spectrum assets and attempting to perhaps get out of the obligations that they have signed. As contracts go, we feel like we have a great contract with them, and it runs through 2036.

And it’s something we think is legally defensible. We recently elected to file a lawsuit in order to fully protect our rights. … We expect them to pay for that contract. If in the future, there was an opportunity to go and have a negotiated settlement, it would have to be something that made good sense for ourselves and our shareholders. We’re not looking to let them out of their obligations, but understand that the market would love the surety of putting this behind us.

Then, on January 12 we heard:

“While it initially continued to make its required payments, DISH recently failed to do so and defaulted on its obligations under the agreement with Crown Castle. In an effort to protect its shareholders, Crown Castle exercised its right to terminate the agreement and to recover in excess of $3.5 billion in remaining payments owed.”

The Ongoing Asset Sale

On top of that, Crown Castle got pressured into selling off the third of their business that was focused on fiber solutions and small cells. And that led them to cut the dividend by a third. The sale should close in the first half of this year.

Here is what they said about the uses of the proceeds of the $8.5B sale when they announced it last March:

After closing the Fiber transaction, we expect to use substantial cash proceeds to repay debt. And based on preliminary analysis, we believe the enhanced stability of our free cash flow profile as a pure-play U.S. tower business will allow us to maintain an investment-grade credit rating with a target leverage between 6 and 6.5x.

Finally, we expect to repurchase shares. Currently, Crown Castle intends to implement the share repurchase program of approximately $3 billion in conjunction with the close of the transaction, which we expect to happen again in the first half of 2026.

At today’s low stock price, that $3B will represent 8% of the float. So the net impact of the sale seems to be that selling assets that produced a third of the CfO led to an increase in leverage and a reduction of the CfO/share by more than a quarter.

It does not matter now whether this made any sense. Those assets are sold and Crown Castle has new management. Here is what they said about their current priorities in the Q3 earnings call (edited for length):

Fundamentally, we will be focusing in on back to basics to maximize the revenue opportunities that we have within the existing portfolio.

Following the close of our sale transaction, we intend to grow our dividend in line with AFFO, excluding amortization of prepaid rent by maintaining a payout ratio of 75% to 80%. Additionally, we continue to expect to spend between $150 million to $250 million of annual net capital expenditures to add and modify our towers, purchase land under our towers and invest in technology to enhance and automate our systems and processes.

That capex will run in the ballpark of 10% of AFFO. So maybe these numbers work. (That capex is also small enough that for this rough analysis we will ignore closer examination.)

Financials and Multiple

It does not look to me as though Adjusted Funds From Operations (AFFO) is particularly misleading for this firm. Because of their lease escalators, there are some significant non-cash items that need to be taken out of FFO.

But we don’t yet have forward guidance for post-sale numbers. And as always for a thorough analysis my preference is to track Cash from Operations (CfO).

Crown Castle’s leases typically have fixed 3% rent escalators and very long terms. In addition, since their towers can accommodate several tenants and usually start with one. The average now is at 2.4.

When they are not losing tenants, this adds a tailwind to earnings growth. Today their towers built before 2007 are producing 50% more revenue on average than those built after 2006.

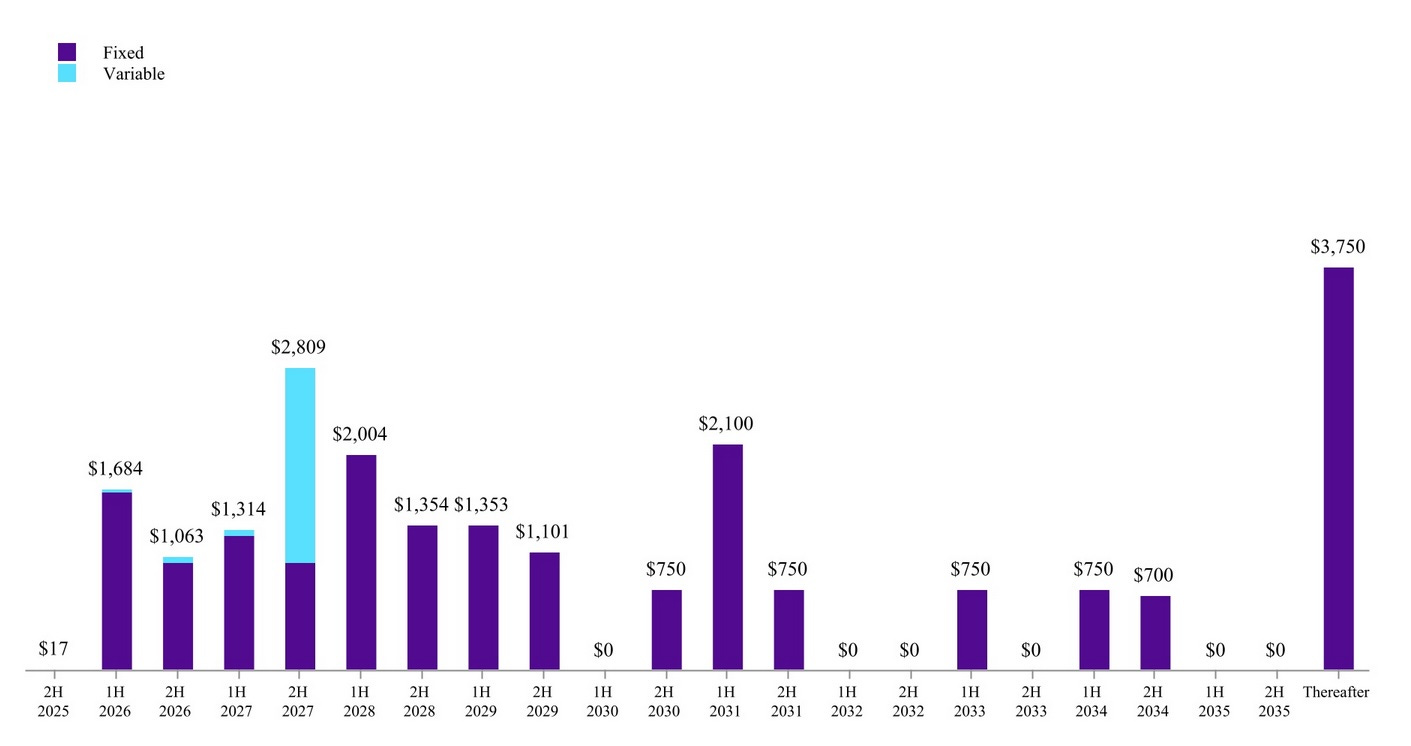

Their debt is very nicely laddered:

Crown Castle is now rated BBB or BBB+, but agencies are skeptical of the asset sale. While a lot of their debt is at high enough interest rates that it will not be painful to replace, some of it will be.

Here are numbers based on current debt; debt will decrease after their asset sale: If long rates stay near where they are, Crown Castle would see interest expense increases in the ballpark of $30M in 2026, $8M in 2027, and $60M in 2031. Compare that to the current annual expense of about $900M. Pro-forma CfO will be near $2B, so this ballpark would look like a headwind to growth of 1.5% in 2026, much less in 2027, and 3% in 2031.

The bottom line is that Crown Castle should be able to grow their Net Operating Income at a few percent per year based mainly on their escalators. They may do better if strong demand for bandwidth really is sustained.

Crown Castle had been bragging for years that they foresaw dividend growth near 8% throughout the 5G transformation. The hit to revenues from the Sprint cancellations led dividend growth to drop from around 8% to nothing starting in 2023. Dividend growth over the past decade is only 20%, on net.

The CCI stock price looks down on that graphic above, but it is still priced near 30x the post-sale AFFO (and CfO). So even today this is pricing in rapid growth.

Takeaways

With so few tenants in a tumultuous industry, this stock does not look like a safe bet to me. It would be no surprise to see some good years now again followed by some kind of turmoil that will again squelch the dividend and long-term returns.

The markets are demanding a 5% yield today, 80 bps less than NNN REIT (NNN) does. I vastly prefer NNN. The yield is also over 140 bps less than one can get from VICI Properties (VICI) or EPR Properties (EPR). My feelings about both, and especially EPR, are that the present yield is not high enough to compensate for the risks.

So if you buy it, you might do well with this stock. But it is not for me.

Please click that ♡ button. This helps push Focused Investing up on the Substack feed. And please subscribe, restack, and share. Thanks!

Great analysis. I own a fair amount of CCI but after reading your analysis I will pause adding more. Hopefully you can do a piece for HYL to cover CCI, SBAC, and AMT.

Thx Paul. I only occasionally dabble in REITdom, but this one will not be one if them.